Alibaba Group (BABA, 09988), Tencent (00700), and their peers have recently suffered some of the worst sell-off episodes since their listing, following probes on their anti-competition practices, data security, and social responsibility. At the end of 2021, Alibaba inched close to its 5-year lows while Tencent’s stock price completely wiped-out gains accumulated since mid-2021, down nearly 40% from the peak. Trading at these levels, are they worth reconsidering in 2022 and beyond?

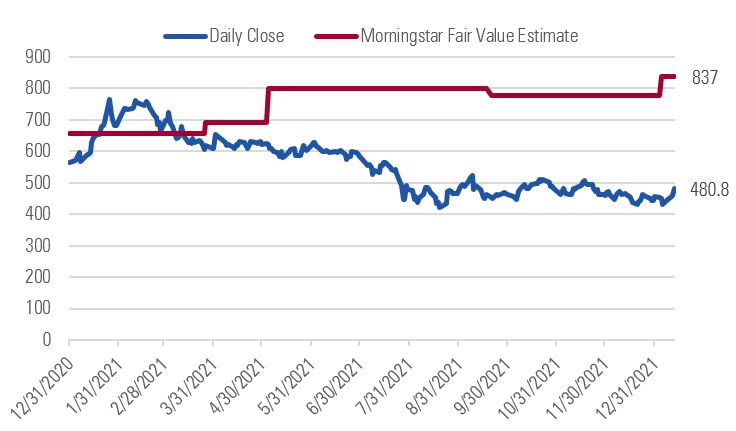

Stock Price Correction of Alibaba and Tencent

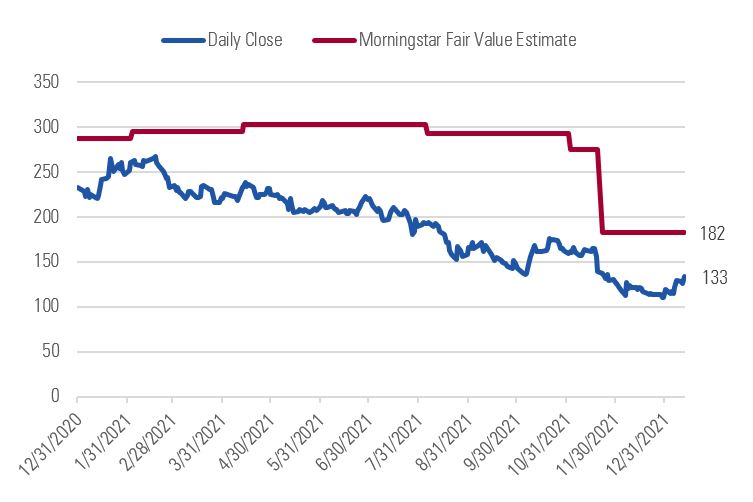

Shares in Alibaba slid 60% from its 2020 peak, while Tencent retreated nearly 40%.

New Sector Rules

Investor sentiment continues to remain fearful of large-scale Chinese tech firms after the regulatory probes crushed the shares. The stocks continue to trade range-bound around their recent troughs. Morningstar’s senior equity analyst, Ivan Su believes the regulator’s actions in cleaning up malpractices in the fast-expanding internet and tech sector reminds investors of the private tutoring industry.

However, this should not be the case. Su calls out the differences between tech and education. “While we understand that some of these changes give investors flashbacks to what has happened in the Chinese education sector, it is essential to understand that recent Internet regulations are not designed to wipe out the Internet industry or the private sector, nor will they erode the competitive advantages enjoyed by Tencent.”

He believes the market has “dramatically overreacted” to recent regulatory risks while overlooking the firm’s long-term revenue opportunities and margin upside. Therefore, he remains steadfast on the wide-moat firm, citing its fundamental strength staying intact. According to his research, Tencent’s moat source derives from its ability to monetize its network effects around its massive user base on the all-in-one messenger platform, WeChat. Tencent also possesses moat sources like intangible assets, mainly from its well-known mobile game franchise.

Higher Conviction on Mobile Games

Looking ahead, Su sees signs of a stabilizing—or even an improving –regulatory environment going into 2022. From China’s latest Politburo meeting, Su spots a positive sign from comments, where "anti-monopoly" and “preventing disorderly expansion of capital,” which made their first appearance in last year's December meeting, were taken out from this year’s address. “We view this as an indication that anti-monopoly will no longer be a top government priority in 2022,” says Su. “We have confidence that fears will subside as investors gradually understand headline risks do not represent fundamental game-changers to our long-term investment theses.”

Tencent’s fair value estimate is revised upward to HKD 837 from HKD 778, representing at least 44% upside.

Su explains that the revision is to reflect a more rosy profitability outlook for the firm’s gaming business. The long-term conviction is underpinned by three secular trends: 1) rising value proposition of online games (easy to access and highly engaging way to enjoy with friends), 2) rapidly growing disposable income bodes well for advertising spend, and 3) surging demand for cost-effective enterprise solutions provides ample of headroom for cloud services growth.

Intensifying Competition

Chelsey Tam, senior analyst who covers e-commerce giant Alibaba, retains the fair value estimate of HKD 182 (USD188) for the stock. The outlook for Alibaba looks more challenging due to the competitive landscape at home and abroad. Tam says: “Alibaba still needs to be able to identify and meet the fast-changing consumer demands quickly, offering affordable products and services to consumers in less developed areas. We think Alibaba’s execution in meeting these demands is not solid.” She points to one common characteristic that rivals Pinduoduo and Douyin possess and Alibaba does not - access to strong traffic at lower customer acquisition costs. Moreover, despite a manifest commitment to developing the remote areas, Alibaba appears to have made few inroads into the less developed markets.

The pain point for Alibaba’s strategy for the coming years will be that the company is under intense competition in the unprofitable and low end of the e-commerce market in China that it must enter in order to achieve its goal to be the omnichannel retail giant in China.

For this segment, Tam expects it to cost Alibaba more than originally estimated to get to those new customers in the lower-tier cities and emerging markets overseas. While Alibaba still holds an exemplary rating in capital allocation, Tam points to evidence that its domestic and international business leadership is being shaken by a spate of contenders, especially in the Southeast Asia markets. “We are also less optimistic about Alibaba’s long-term growth due to the trend of consumers making purchases in an increasing number of channels.”

Alibaba’s Share Price and Fair Value Estimate

©2021 Morningstar. All rights reserved. The information, data, analyses and opinions presented herein do not constitute investment advice; are provided as of the date written, solely for informational purposes; and subject to change at any time without notice. This content is not an offer to buy or sell any particular security and is not warranted to be correct, complete or accurate. Past performance is not a guarantee of future results. The Morningstar name and logo are registered marks of Morningstar, Inc. This article includes proprietary materials of Morningstar; reproduction, transcription or other use, by any means, in whole or in part, without prior, written consent of Morningstar is prohibited. This article is intended for general circulation, and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. Investors should consult a financial adviser regarding the suitability of any investment product, taking into account their specific investment objectives, financial situation or particular needs, before making any investment decisions. Morningstar Investment Management Asia Limited is licensed and regulated by the Hong Kong Securities and Futures Commission to provide investment research and investment advisory services to professional investors only. Morningstar Investment Adviser Singapore Pte. Limited is licensed by the Monetary Authority of Singapore to provide financial advisory services in Singapore. Either Morningstar Investment Management Asia Limited or Morningstar Investment Adviser Singapore Pte. Limited will be the entity responsible for the creation and distribution of the research services described in this article.

.png)

.jpg "Kate Lin")