The Chinese government continues to work on improving social stability and economic longevity. One of its favourite targets has been the video game industry. In addition to the rule that caps minors’ weekly gaming hours to a maximum of three hours, the National Press and Publication Administration, which clears video game launches, does not grant any licenses for August.

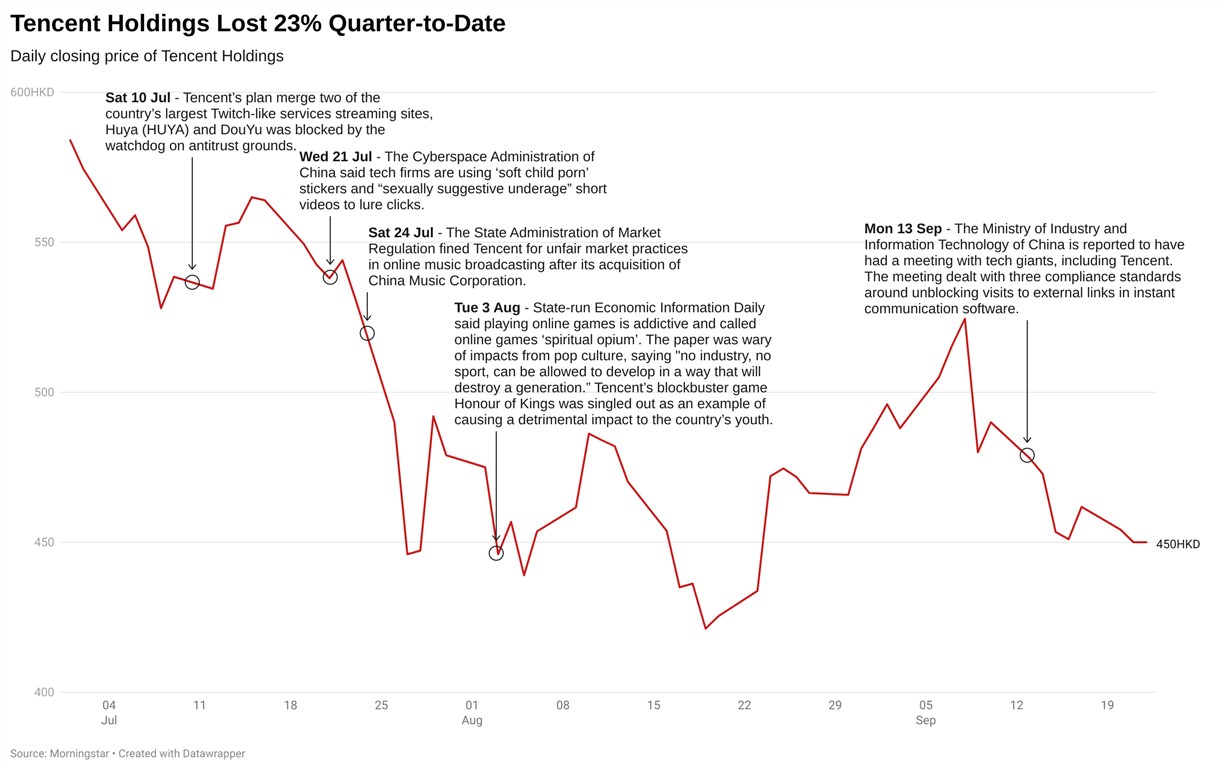

At least four of Tencent’s businesses were hit by this. Here is a timeline of the regulatory actions so far.

Potential Delay

The latest blow was to Tencent’s flourishing online game business, as the watchdog for game approvals did not release new licenses. Tencent’s next key game, DNF mobile is in the queue to get a license. For now, it is unclear when this delay in new game licenses will ease.

Chelsey Tam, senior equity analyst at Morningstar, sees it as a sign that the Chinese government has suspended game launches, which has happened before. “We assume games won’t be approved for 10 months this time, similar to the duration of game approval suspension in 2018, followed by three to four months of testing and preparation for game launches.”

That means, DNF mobile, developed by Tencent’s partner Nexon in South Korea, will have to wait until the fourth quarter of 2022 to receive the greenlight. Tencent will have to postpone the launch for at least one year, not factoring in the period for closed testing.

Another game in the launch pipeline is League of Legends: Wild Rift (LoL). Tencent is the publisher of the game. Although the approval for LoL was granted in February 2021, Tam believes the game will have to be delayed assuage officials that the firm is aligned with the country’s goal to ensure minor protection. Its launch could be delayed to after the National Holiday in October.

Financial Impacts

For the game projects that are sidelined, Tam assumes an immediate impact on the profit estimates for 2021. Overall, Tam trims Tencent's online game revenue forecast by 7% and 8% for 2021 and lowers her fair value estimate by 3% to HKD 778 from HKD 800. Despite the trim, Tencent's still trading a deep discount versus its fair value estimates, based on its last market close of HK$ 450.

Tam retains her estimates of revenue contribution from the young gamers to stay around low single digits.

“We think there is some downside from cracking down on minors that use adult accounts to play games but given minors do not have income, they are unlikely to generate a material amount of gaming revenue,” says Tam. She expects to see mix shift toward offline games, for example, certain single-player games that can offset some of the impacts.

Longer-Term Views

At Morningstar, we emphasize a long-term investment horizon that takes into account valuation and the future opportunities for the stocks. Tam believes it is more likely than not that these stocks will bounce back in a few years. She underscores some upside potential that is overshadowed by investors’ panic, reflecting in the beaten-down share prices.

She envisions that the increasingly stringent requirement at home would encourage these game developers to look beyond the border. “The long-term potential for these quality game designers and distributors is to cross the border to diversify their business focus. While risks continue to loom around the domestic market, gaming firms may put international expansion in a higher priority than prior and speed up building their franchises on the mobile and PC gaming stores overseas.”

Before the official’s talk with the game companies in early September, another game developer and publisher NetEase (09999) received a significant increase in fair value estimate at the end of August, to HK$217 per share from HK$142, or an 52.8% rise. Tam, who assigns the estimate, says she maintains her outlook amid the evolving regulations.

“The bulk of the increase comes from our updated outlook for higher long-term growth and profitability in the gaming segment. The overreaction by the market to the recent risks shows that the market is somewhat overlooking the firm’s long-term opportunities overseas.” Morningstar views the narrow-moat company, which closed HK$124.9 on Tuesday, as undervalued.

©2021 Morningstar. All rights reserved. The information, data, analyses and opinions presented herein do not constitute investment advice; are provided as of the date written, solely for informational purposes; and subject to change at any time without notice. This content is not an offer to buy or sell any particular security and is not warranted to be correct, complete or accurate. Past performance is not a guarantee of future results. The Morningstar name and logo are registered marks of Morningstar, Inc. This article includes proprietary materials of Morningstar; reproduction, transcription or other use, by any means, in whole or in part, without prior, written consent of Morningstar is prohibited. This article is intended for general circulation, and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. Investors should consult a financial adviser regarding the suitability of any investment product, taking into account their specific investment objectives, financial situation or particular needs, before making any investment decisions. Morningstar Investment Management Asia Limited is licensed and regulated by the Hong Kong Securities and Futures Commission to provide investment research and investment advisory services to professional investors only. Morningstar Investment Adviser Singapore Pte. Limited is licensed by the Monetary Authority of Singapore to provide financial advisory services in Singapore. Either Morningstar Investment Management Asia Limited or Morningstar Investment Adviser Singapore Pte. Limited will be the entity responsible for the creation and distribution of the research services described in this article.

.png)

.jpg "Kate Lin")