Guaranteed funds, the third-largest slice of MPF assets, gathered more than HK$700 million (US$90.2 million) from Hong Kong workers as of the end of last month. Guaranteed funds’ conservative risk profile can benefit to your future retirement pot, but the strategy is not defined for every life stage.

Know What You Own

It is important to first understand how MPF managers design guaranteed funds and what can be guaranteed.

By Morningstar’s definition, guaranteed funds are offered in two flavors. They either guarantee the repayment of invested capital (either all or in-part), or promise a pre-determined rate of return.

Having your capital preserved is great, but unlike promises we make to our loved ones, this promise comes with a price and conditions.

A guarantor, usually an insurer, charges a fee for the managing risks. This charge is added to the management fee. As a result, guaranteed funds are more expensive than most of the low-risk fund categories.

The guarantee offered is conditional and can vary from one fund to another depending on the investment objective stated in the prospectus.

For example, the guaranteed return will not be applicable if investors withdraw before the minimum holding period or make lower contributions than are required. Guarantors may also be allowed to cancel the guarantee at their discretion if they provide advanced notice. In certain cases, they can remove the promised safety net, say in the face of unfavorable market conditions, where protection of capital is the most the most needed.

Are Guaranteed Funds Worth Considering?

Considering all these drawbacks, is a guaranteed fund still a worthwhile investment option?

It depends, but the conclusion takes more than ‘promises’ to make.

Most younger contributors can assume wealth to accumulate steadily over time. For a period long enough, one’s human capital, which is the ability to earn money over time, has room to grow. Such expectations ultimately impact how one would allocate MPF investments. With many income-earning years ahead, an investor can take on more risk with a more aggressive allocation.

The ‘guaranteed’ feature typically appeals to those who are still on the job but are planning for an imminent retirement. Until they are eligible for a withdrawal, the promised returns and guaranteed capital invested provide a favorable margin of safety.

Guaranteed funds usually are less risky (as measured by standard deviation) than the market average, but they bear some unique risks that aren’t taken on in other MPF categories. For instance, the failure of a guarantor can lead to a return that falls short of expectations. Furthermore, guarantors with an insurance background add credit risk to the investment.

Alternatives for Consideration

Lastly, for those who have already allocated MPF assets to guaranteed funds, a regular portfolio check-in may be worthwhile to keep up with any changes in the terms. Before switching MPF managers, make sure you read through the terms and conditions to avoid giving up the promised returns.

As said, guaranteed funds incur additional fees and their terms can vary. Here are two aspects one can consider.

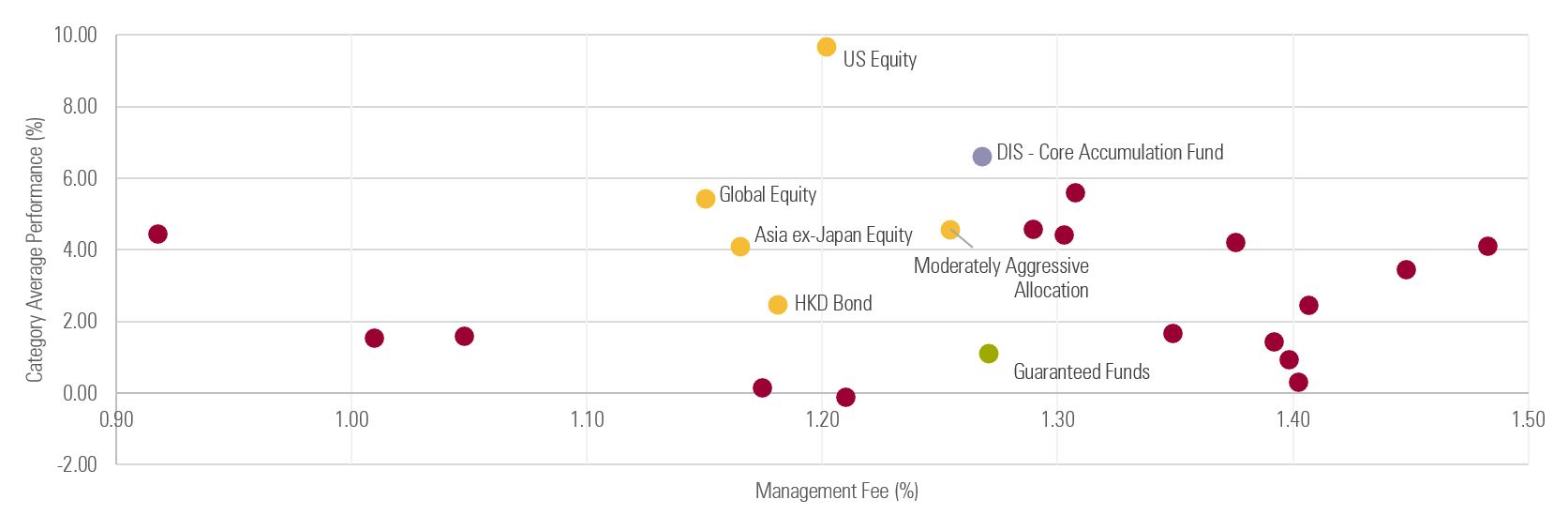

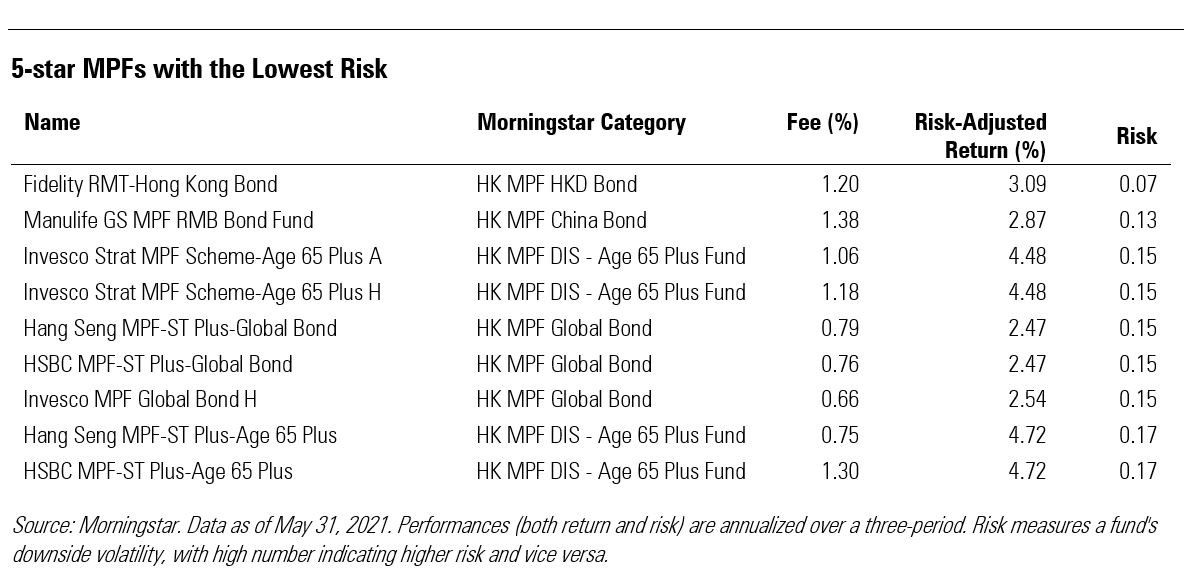

If fee is a top concern in constructing a MPF portfolio, there is a range of cheaper alternatives (in yellow mark) that generate a better risk-adjusted return over the past three years versus guaranteed funds.

Category Performance/Fee Comparison

Moreover, in building a low-volatility MPF portfolio, investors can compare risk-adjusted return and risk among individual funds or among MPF categories. Volatility of guaranteed funds, as measured as standard deviation, typically ranges between 0% and 0.4%. Selective bond and mixed assets MPFs are a cheaper alternative for conservative investors who want to get around wordy terms and conditions. Bonds share some risk-return features with guaranteed funds, though without any guarantees on principal. The Age 65 Plus Funds are globally diversified portfolios. They invest 80% of total assets in low-risk assets, mainly global bonds and the remaining of assets goes into higher-risk equities, which allows these funds to deliver higher than guaranteed funds with the same level of risk.

©2021 Morningstar. All rights reserved. The information, data, analyses and opinions presented herein do not constitute investment advice; are provided as of the date written, solely for informational purposes; and subject to change at any time without notice. This content is not an offer to buy or sell any particular security and is not warranted to be correct, complete or accurate. Past performance is not a guarantee of future results. The Morningstar name and logo are registered marks of Morningstar, Inc. This article includes proprietary materials of Morningstar; reproduction, transcription or other use, by any means, in whole or in part, without prior, written consent of Morningstar is prohibited. This article is intended for general circulation, and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. Investors should consult a financial adviser regarding the suitability of any investment product, taking into account their specific investment objectives, financial situation or particular needs, before making any investment decisions. Morningstar Investment Management Asia Limited is licensed and regulated by the Hong Kong Securities and Futures Commission to provide investment research and investment advisory services to professional investors only. Morningstar Investment Adviser Singapore Pte. Limited is licensed by the Monetary Authority of Singapore to provide financial advisory services in Singapore. Either Morningstar Investment Management Asia Limited or Morningstar Investment Adviser Singapore Pte. Limited will be the entity responsible for the creation and distribution of the research services described in this article.

.png)

.jpg "Kate Lin")