Chinese banks had an unimpressive first quarter. The rebound in net profit growth fell short of market expectations, and net interest margin declined due to pressure in interest rate repricing, a high base in the net interest margins, and low operating expenses in the first quarter of 2020.

But Morningstar analysts believe there will be a gradual improvement of bank profits through the rest of the year. Iris Tan, our senior equity analyst, says the first-quarter results may have marked the low point and the banks under her coverage will see growth of 7.1% in net profit in 2021.

Improving Credit Demand and Quality

There are few industry trends that should translate to a continuous earnings recovery for banks.

First, the economic recovery backs lenders’ profitability, and the loan book of Chinese banks indicates that they are on track to benefit from this stage of recovery, according to Tan.

“We've seen strong growth in corporate mid- to long-term loans since mid-2020 and we expect this trend to continue,” she says. “Management in certain large banks noted very strong credit demand in 2021. Our estimate is an average mean loan growth of 11%.”

Apart from the increasing demand for credit, the loan mix and credit quality are turning for the better. Banks are seen increasing loan allocations to higher-yield retail loans and mid- to long-term corporate loans. This favorable loan mix shall offer some upsides to their overall asset yield.

Tan says: “The economic recovery should help lower credit risks. We note that China has been relatively financially prudent in its pandemic relief and the government is keen to keep debt levels contained. As business activities continue to return normal, we shall see near-term improvement in credit quality.”

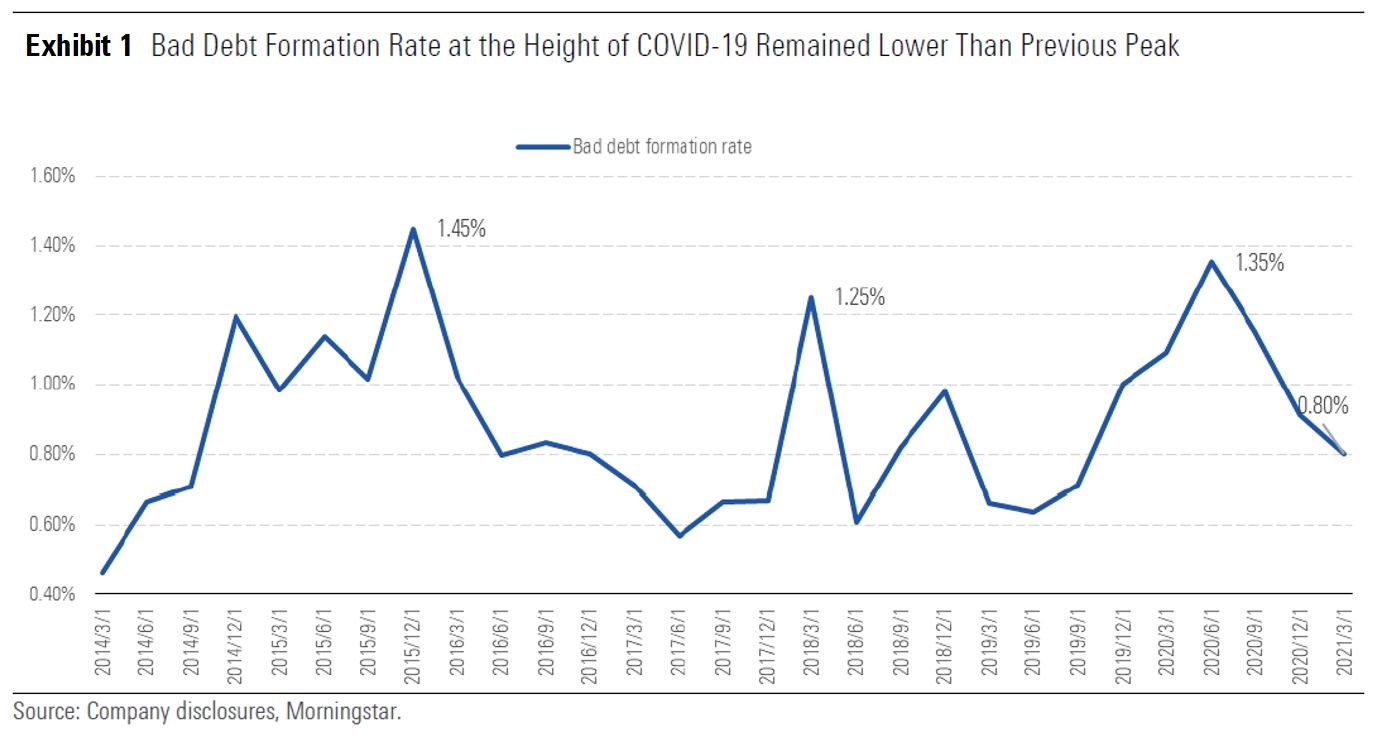

The overall bad debt formation rate further dropped in the first quarter, after peaking at 1.35% in mid-2020. While loan risks are mitigated, banks were able to improve provision levels.

On the policy front, the Chinese government softened the tone on its top-down policy goal to lower financing costs for corporate loans, placing less pressure on loan pricing among banks. Interest rates are anticipated to trend higher in the coming quarters. This contributes to an increase in net interest margins, also benefitting the China banks in our coverage.

3 Undervalued Picks

Chinese banks as a sector benefited from the rotation into financials since October 2020. The Hang Seng Mainland Banks Index, tracking the 10 largest H-shares Chinese banks, rebounded 15.4% year to May this year, following a 13.2% decline in 2020.

After the catch-up rally, Tan still sees room for the China banks. “Except for China Merchant Bank, China banks in our coverage are trading at 0.45 times price/fair value. That means, the group remains collectively attractive and we think that there is still a way to go.” Among them, she has a fundamental preference for the H-shares of three of the larger state-owned banks.

Exhibit 2: Valuation and Metrics for the Bank Picks

|

|

CCB |

ABC |

ICBC |

|

Valuation |

22% discount |

27% discount |

23% discount |

|

Price/Book Ratio |

0.5x |

|

0.5x |

|

Forward Dividend Yield |

6.2% |

7.1% |

6.3% |

Source: Morningstar Direct. All data is quoted for H-share listing as of June 9, 2021.

China Construction Bank (00939)

The bank has the highest share of low-risk loans, including government-led infrastructure-related loans and home mortgages, which account for over 60% of total loans. The bank adopts very strict bad debt recognition standards and it has recognized all overdue loans as bad debts.

Agricultural Bank of China (01288)

The undervaluation of ABC mainly comes from the market’s overblown concerns on its asset quality. Our analysts have found that the bank has effectively cleaned up its balance sheet from 2017, improving its bad debt ratio and being more transparent of asset quality. Its bad debt ratio declined to 1.57% in 2020 from 2.19% in 2017. ABC has a strong rural deposit base, and its offline distribution network is the largest in the country. These enable the bank to benefit from the regulatory trend of eliminating smaller banks’ presence in the rural market.

Industrial and Commercial Bank of China (01398)

ICBC’s funding costs advantage, quality customer base, and operating efficiency are the differentiators for it to better fend off challenges of lower interest rates. Its leading branding, network and capital in mass market banking has created high entry barriers for most peers. Furthermore, its asset management arm continues to capitalize on its extensive distribution network and a solid lineup of insurance, fund and securities brokerage businesses.

Booming Wealth Trend

A broad industry trend to play for the long haul is the liberation of the country’s massive spending pool and bourgeoning middle class. As a result, the wealth management business in China is expected to accelerate in 2021 onwards, becoming the most critical driver for the time to come.

The private wealth business model is human-centric. Intangible assets like client relationship and talents directly point to a bank’s moat, which Morningstar believes is the most durable sources of competitive advantages in this context. Thus, the industry leaders with established scale would be more capable in absorbing market share from the expanding market.

Our preferred picks of CCB and ICBC stand to be beneficiaries of this market after the cleanup of their legacy bank wealth management products. Other than that, fairly-valued China Merchants Bank (03968) and Ping An Bank (000001) are best positioned to capture the growth. This is because “both banks enjoy a strong premium retail customer base, and this is the key to capture the quickening growth in fee-based income.”

©2021 Morningstar. All rights reserved. The information, data, analyses and opinions presented herein do not constitute investment advice; are provided as of the date written, solely for informational purposes; and subject to change at any time without notice. This content is not an offer to buy or sell any particular security and is not warranted to be correct, complete or accurate. Past performance is not a guarantee of future results. The Morningstar name and logo are registered marks of Morningstar, Inc. This article includes proprietary materials of Morningstar; reproduction, transcription or other use, by any means, in whole or in part, without prior, written consent of Morningstar is prohibited. This article is intended for general circulation, and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. Investors should consult a financial adviser regarding the suitability of any investment product, taking into account their specific investment objectives, financial situation or particular needs, before making any investment decisions. Morningstar Investment Management Asia Limited is licensed and regulated by the Hong Kong Securities and Futures Commission to provide investment research and investment advisory services to professional investors only. Morningstar Investment Adviser Singapore Pte. Limited is licensed by the Monetary Authority of Singapore to provide financial advisory services in Singapore. Either Morningstar Investment Management Asia Limited or Morningstar Investment Adviser Singapore Pte. Limited will be the entity responsible for the creation and distribution of the research services described in this article.

.png)

.jpg "Kate Lin")