After a long, dark, cold winter, green shoots have emerged across the landscape of systematic value strategies—those that buy stocks that are cheap relative to some fundamental measure of their worth. Exactly what has plagued these approaches for so long has been widely debated. And while the recent thaw has been welcomed by many long-suffering value disciples, even some of the factor’s biggest fans worry that it may be a false spring.

Here, I’ll look back at value’s cold streak, survey some of its potential causes, touch on the catalysts behind its turnaround, and explore whether there’s any value left in value today.

What Happened?

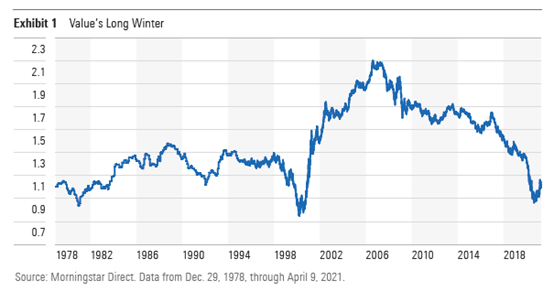

Exhibit 1 is a relative wealth chart. It plots the growth of an investment in the Russell 3000 Value Index versus an investment in the Russell 3000 Growth Index from their shared inception on Dec. 29, 1978. When the line slopes upward, it indicates that the value index outperformed the growth index, and vice versa. From their inception through Aug. 8, 2006 (the peak in the relative amount of wealth created by an investment in the value index versus the growth index), the value benchmark outperformed its growth counterpart by 3.02 percentage points annually. Since then, the tide has turned. From that August 2006 peak through April 11, 2021, the value index lagged the growth index by 5.61 percentage points a year. What happened?

Academics and practitioners have published numerous studies attempting to explain why value stocks have underperformed their faster-growing and more richly priced counterparts for so long.

Some have argued that traditional measures of value like the book value of equity are no longer a reliable gauge of companies’ worth, as modern enterprises’ assets skew away from plant and equipment and toward intellectual property and goodwill.

Others have tried to peg value’s woes on interest rates, arguing that low rates are better for companies whose best days and biggest cash flows are further out in the future. These stocks’ premium multiples may be justified by lower discount rates on those further-out cash flows, which boost their present value.

Another narrative—one that may be familiar to those who lived through the dot-com bubble—is that value stocks are systematically short innovation. By focusing on accounting measures for stock selection, they’re driving using the rearview mirror, favoring old industry, and failing to see and participate in all the disruption that is coming down the road.

If you ask me, most of these arguments hold little water. The factors affecting stock prices and the relative performance of those stocks trading cheap in relation to accounting measures and their more glamorous counterparts are too numerous to count.

The manner in which these factors interact is complex. It is impossible to predict how they will conspire to move markets ahead of time. And it is easy to try to explain how they affected prices with the benefit of hindsight and mounds of data.

Amid all this complexity are two relatively simple factors that I believe explain most of value’s woes: fundamentals and people.

For most of value’s long drought, it deserved to be left in the dust by growth. This is because growth stocks’ earnings grew at a much faster rate during most of this period. But the difference in earnings growth rates has narrowed. That’s where people come in. When I say “people” I am referring to investor behavior, animal spirits, all those touchy-feely factors that have driven many a market mania and panic over the years. This is evidenced in the expansion of growth stocks’ multiples relative to the going price for value stocks. Exhibit 2 depicts the ratio of the price/earnings multiple for the Russell 3000 Growth E Index to the price/earnings multiple for the Russell 3000 Value E Index. By definition, growth stocks tend to garner higher multiples relative to value stocks. But that premium has spiked higher in the past few years. Investors have thrown valuations to the wind, paying up for the market’s fastest-growing names.

In part 2 of this article, we will continue to explore whether value strategies have a comeback.

©2021 Morningstar. All rights reserved. The information, data, analyses and opinions presented herein do not constitute investment advice; are provided as of the date written, solely for informational purposes; and subject to change at any time without notice. This content is not an offer to buy or sell any particular security and is not warranted to be correct, complete or accurate. Past performance is not a guarantee of future results. The Morningstar name and logo are registered marks of Morningstar, Inc. This article includes proprietary materials of Morningstar; reproduction, transcription or other use, by any means, in whole or in part, without prior, written consent of Morningstar is prohibited. This article is intended for general circulation, and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. Investors should consult a financial adviser regarding the suitability of any investment product, taking into account their specific investment objectives, financial situation or particular needs, before making any investment decisions. Morningstar Investment Management Asia Limited is licensed and regulated by the Hong Kong Securities and Futures Commission to provide investment research and investment advisory services to professional investors only. Morningstar Investment Adviser Singapore Pte. Limited is licensed by the Monetary Authority of Singapore to provide financial advisory services in Singapore. Either Morningstar Investment Management Asia Limited or Morningstar Investment Adviser Singapore Pte. Limited will be the entity responsible for the creation and distribution of the research services described in this article.

.png)